Global VC deals slipped further in Q2 | Pitchbook

4 min read

[ad_1]

Missed the GamesBeat Summit excitement? Don’t worry! Tune in now to catch all of the live and virtual sessions here.

Global venture capital deal counts took a dip in Q2, after several quarters of a plateau as both Europe and Asia investments slowed during the quarter, Pitchbook said. Global exits were the lowest since the first quarter of 2018.

Europe and Asia activity slowed during the quarter, pressuring the total figure downward. The value of completed deals has plateaued now for a few quarters, well below the highs of a couple years ago.

Without large investors (crossover investors, private equity firms, and sovereign wealth funds) actively participating in venture, the outsized deals that pushed deal value to records aren’t able to get done, according to a first look of a Q2 report by Pitchbook.

Exit activity continues at subdued levels, and the $51 billion of global exit value was the second lowest since Q1 2018. Public market opportunities are low, and the more active antitrust scrutiny has kept large acquisitions sidelined as well, Pitchbook said. Global inflation and heightened geo-political tensions amongst key venture markets have also put pressure on exits.

Event

Transform 2023

Join us in San Francisco on July 11-12, where top executives will share how they have integrated and optimized AI investments for success and avoided common pitfalls.

Slow fundraising in Europe and North America is pressuring global fundraising totals lower for the year. Asia fundraising, on both a fund count and fund value basis, is roughly on pace with 2022, though much lower than seen in 2021. A poor exit market globally will continue to offer a poor market for general partners raising funds, as limited partners are receiving low distributions to recycle into the venture strategy.

U.S. key takeaways

Pitchbook said U.S. deal activity has been flat over the past few quarters, remaining elevated above pre-2021 levels, despite the swift decline seen from the end of 2021 and early 2022 figures.

Pitchbook estimates show that both early-stage and venture growth saw deal count increases in Q2, though deal value for both continues to be much lower than anticipated. What this tells us is that likely many of these deals are being used to increase cash runways with as little dilution as possible, rather than raise a full round in a down market, Pitchbook said.

Exit value is on pace to finish the year just over $20 billion, which would be the lowest in the past decade by almost $50 billion. Intial public offerings have not been viable options for VC-backed companies this year, despite the public markets showing positive returns on the year.

Companies that arose under the growth-at-all-costs mantra still need time to restructure their business models in a way that public market investors are willing to place a premium on, such as a well-developed path to profitability.

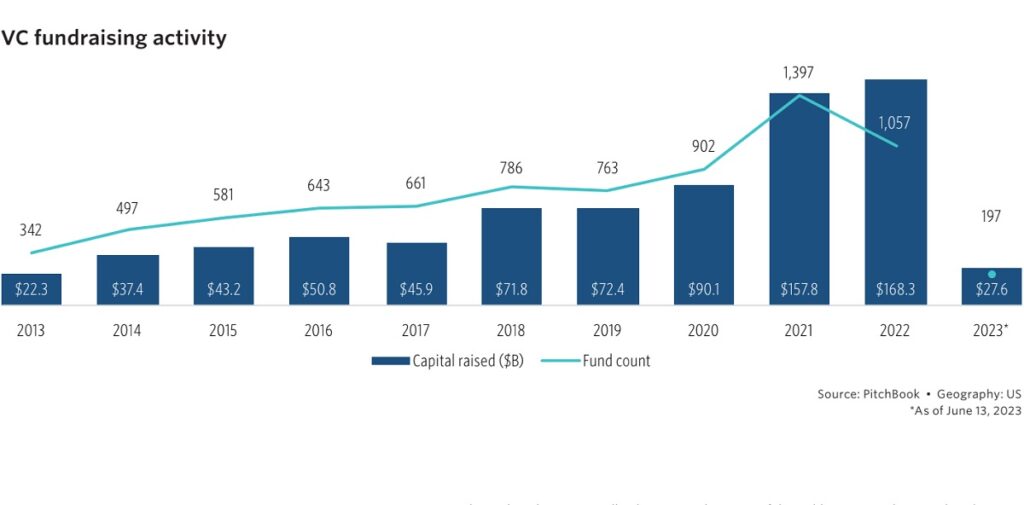

Fundraising received a boost in Q2, with several large funds closing, but at $33 billion, the year is on pace for the lowest fundraising total since 2017. More then 3,600 funds have now closed since the beginning of 2020, keeping deal counts relatively high as there remains a high number of funds active in the market. Many GPs have pushed new fundraises out to 2024, as that vintage is seen as a likely rebound for returns.

Europe’s decline in VC deals

European VC deal value continued to decline in Q2 2023 as the dealmaking environment remained sluggish. Deal count fell from the first quarter, as fewer deals were completed amid the current slump.

Longer due diligence processes, scarcer capital availability, and funding runway management are impacting deal activity in the VC ecosystem. Meanwhile, macroeconomic issues including stubbornly high inflation, low economic growth, and high-interest rates continue to dampen broader financial market sentiment in Europe.

Exit activity in Europe stalled in Q2 2023 with few VC-backed companies willing to seek liquidity given unfavorable market conditions. With valuation uncertainty and volatility in public markets, startups and investors are holding off exit plans until further clarity is established. Large exits and public listings have been rare in 2023, and this could persist in H2 2023, Pitchbook said.

Fundraising slowed in in the first half of 2023 with capital raised and the number of closed funds dropping from the pace set in 2022. Tougher fundraising conditions have emerged in the past 12 months and general partners are unlikely to be raising capital at the same rate as recent years. Moreover, limited partners will be prioritizing commitments for potentially lower-risk funds linked to established fund managers with strong track records.

Overall, for the first half of 2023, the Morningstar-Pitchbook U.S. Unicorn Index is expected to show a negative return this year. And series C and D round will likely see the most down rounds, as these companies are the most starved for capital.

The seed-stage valuations and deal sizes will continue their ascent, reaching new annual highs despite a slowdown in total deal value and count.

Special purpose acquisition companies, IPOs and mergers will continue to decline, while liquidations will continue to increase in 2023. Venture-growth deal value will fall below $50 billion in the U.S. U.S. VC mega-round activity will fall below 400 deals, hitting a three-year low.

“The market for public listings remains nonexistent, despite the public markets overall showing strong,

positive returns year-to-date. Fundraising, too, has followed up an annual record for commitments with the lowest quarterly commitments in a decade. All of these were relatively foreseeable and continuations of trends that shaped 2022,” Pitchbook said.

And U.S. VC fundraising will fall between $120 billion and $130 billion in 2023.

GamesBeat’s creed when covering the game industry is “where passion meets business.” What does this mean? We want to tell you how the news matters to you — not just as a decision-maker at a game studio, but also as a fan of games. Whether you read our articles, listen to our podcasts, or watch our videos, GamesBeat will help you learn about the industry and enjoy engaging with it. Discover our Briefings.

[ad_2]

Source link